![]()

![]()

![]()

![]()

Books |

How Do We Get a Wage-Price Spiral When Wage Growth Is Slowing?

Sottotitolo:

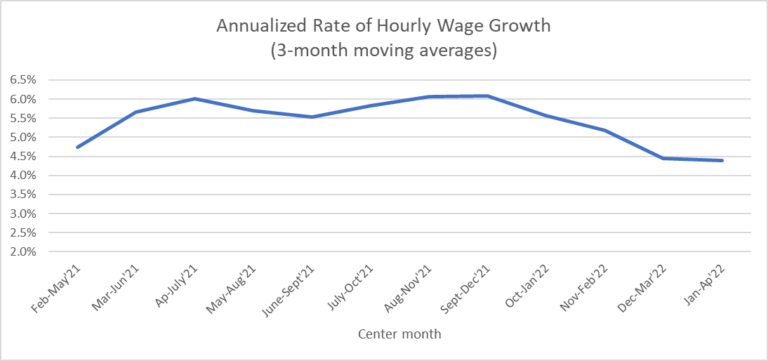

The pattern of wage-growth we are seeing is clearly not consistent with a wage-price spiral story. That’s the question millions are asking, or hopefully at least the folks at the Fed making decisions on interest rates. Ostensibly, the Fed is concerned that the economy is too strong and that we are either on the edge, or already stuck in, the sort of wage-price spiral that led to double digit inflation back in the 1970s. The story back then was that higher prices led workers to demand higher wages, which in turn raised costs and pushed prices still higher. The Fed has begun to raise interest rates to head off this risk. There are many who are urging the Fed to raise rates faster than they have thus far planned, claiming that we are already in this dangerous spiral. The problem with that story is that, rather than spiraling upward, wage growth has actually been slowing in recent months. The chart below shows the annualized rate of growth in the average hourly wage. The calculation is based on three-month averages, where it annualizes the rate of growth between three-month periods

Source: Bureau of Labor Statistics and author’s calculations. As can be seen, the rate of wage growth has slowed sharply this year.[1] After peaking at an annual rate of 6.1 percent between the three-month periods centered on September and December of last year, it has slowed to an annualized rate of just 4.4 in the three-month periods centered on January and April of this year. This is only a percentage point higher than the pre-pandemic rate of wage growth, a period in which the inflation rate was consistently below the Fed’s 2.0 percent target. More importantly, the direction of change has clearly been towards slower wage growth. It is very hard to see how we get a wage price spiral when the rate of wage growth is slowing. To be clear, it is not good to see workers’ wages falling behind inflation. The main villains here are the Ukraine war-related jump in energy and food price, as well as the supply chain issues, which seem to finally be getting resolved. If some sort of peace deal, or at least cease-fire, can be arranged in Ukraine, presumably most of the recent rise in energy and food prices will be reversed. If not, it would be good to have some tax and transfer system so that low- and middle-income people can be compensated for the hit to their living standards. In any case, the pattern of wage-growth we are seeing is clearly not consistent with a wage-price spiral story. The Fed would be making a bad mistake if it raises rates as though it were responding to one. [1] As has been widely noted, the growth rate of the hourly wage is affected by the changing composition of the workforce. When workers in low-paying jobs in sectors, like restaurants and hotels, go back to work, it reduces the measured increase in wage-growth. This would have been more of a factor in the fall, when we were adding close to 600,000 jobs a month, than in more recent months when the rate of job growth has been closer to 400,000. Dean Baker

Dean Baker is the co-director of the Center for Economic and Policy Research (CEPR). He has worked for the World Bank, the Joint Economic Committee of the U.S. Congress, and the OECD's Trade Union Advisory Council. His latest book is "Rigged: How Globalization and the Rules of the Modern Economy Were Structured to Make the Rich Richer" |

https://www.cepr.net/wp-content/uploads/2022/06/Book2_7571_image001-1024... 1024w,

https://www.cepr.net/wp-content/uploads/2022/06/Book2_7571_image001-1024... 1024w, {kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}