![]()

![]()

![]()

![]()

Books |

Financialization and the Jobless Recovery

Sottotitolo:

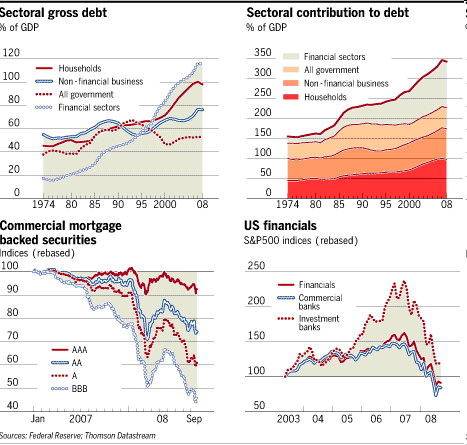

Today, the financial sector has become a primary governance agent and organizer of the real economy. Productivity growth and wage growth have been de-coupled., thus the new growth model is based on debt, not wages, as the source of demand growth. The expansion of financial capitalism provides one deep-rooted cause for the lack of job creation as the US economy recovers from the current financial crisis. Two dimensions of financialization are important: first, the shift to a narrow focus on shareholder value, which places a premium on short-term profits versus long-term growth, sustainability, and employment; and second, the dramatic growth of corporate debt as the source of investment capital. Under managerial capitalism, capitalists made money through investments in productive enterprises and the creation and realization of value through the management of labor – even in the context of increasingly global markets. While shareholder claims were important, they were not the only consideration in corporate decision-making. Today, an increasing proportion of the economy is organized around financial capitalism – in which productive enterprises are bundles of assets to be reconfigured with the goal of maximizing financial returns – not necessarily creating productive enterprises or jobs. The financial sector has become a primary governance agent and organizer of the real economy. It has captured a growing share of corporate profits in both the US and Europe – growing from 25.7 percent to 43 percent in the US between 1973 and 2005 (Palley 2007: 36) Under the new shareholder model of financial capitalism, then, the focus of investment activities has shifted – from that of investing in productive enterprises to that of extracting money from companies in order to pool resources for further trading activities, which yield higher returns. Finance capital follows investment opportunities that the yield the highest returns, regardless of geographic location. In the current recovery, there are few incentives to invest purposefully in enterprises that create jobs, particularly within the confines of the US national economy. The shareholder focus is coupled with a dramatically expanded reliance on debt financing among corporations in the real economy as well as the financial sector. The model of debt financing has diffused broadly across the economy, and corporate profits are increasingly used for stock-buybacks, designed to artificially raise the value of stocks and enrich shareholders, rather than investments to expand productive activity and jobs (Lazonick 2009). The combination of maximizing shareholder value and debt financing has important implications for employment creation. First, the reliance on debt, coupled with asset price inflation, has meant that corporations do not need to rely on employment and wage growth as the source of demand growth – as was the case in the post-war period. Productivity growth and wage growth have been de-coupled. Tom Palley (2009) provides a succinct description of the role of debt-financed spending in the new, neo-liberal growth model as it operates in the U.S.: "In place of wage growth as the engine of demand growth, the new model substituted borrowing and asset price inflation. …The new neo-liberal model was built on financial booms and cheap imports. Financial booms provide consumers and firms with collateral to support debt-financed spending. Borrowing is also sustained by financial innovation and deregulation that ensures a flow of new financial products, allowing increased leverage and widening the range of assets that can be collateralized. Meanwhile, cheap imports ameliorate the impact of wage stagnation, thereby maintaining political support for the model. Additionally, rising wealth and income inequality makes high-end consumption a larger and more important component of economic activity … Thus the new growth model is based on debt, not wages, as the source of demand growth; on asset price inflation and bubble-driven growth; on cheap imports to mitigate wage stagnation so that an over-valued currency and large trade deficit are not seen as a problem; and on financial deregulation and financial innovation to support the growth of debt. This type of growth is, ultimately, unsustainable. Asset bubbles must eventually burst, when someone realizes that a tulip bulb however exotic is, after all, only a tulip bulb." Second, maximizing shareholder value depends importantly on the expanded use of debt to finance investments. Higher levels of corporate debt put pressure on managers to maximize shareholder value via cost cutting and short term strategies. Drawing on agency theory, economists argued that loading up companies with debt would lead to a more efficient allocation of capital and risk. It would raise shareholder value by constraining discretionary management strategies, thus disciplining managers and increasing company earnings. The resulting pressure was expected to raise internal rates of return and earnings per share. Under these conditions, managers are under pressure to achieve short-term profits, and reductions in labor are an important solution. In the current period, even if product demand picks up, employers are likely to rely on overtime hours or temporary work, not new hiring. The impact of new financial intermediaries In addition to the management fees that may total millions of dollars, these firms make money in three ways: by increasing operating revenues via improved performance or reduced costs; by financial engineering, for example, by selling property assets and using the proceeds for dividends and distributions to general and limited partners; or by selling the company at higher earnings multiples compared to its initial purchase price – either because operating revenues have improved or because stock prices have risen across the board. In the 2000s -- with low interest rates, easy access to borrowed funds, a bullish stock market, and a real estate bubble– private equity relied primarily on financial engineering and rising stock market multiples to make money. The global financial crisis together with the long recession of 2008-2009 and the slow recovery from both have created challenges for the PE business model. Private equity firms have ignored the risks of financial distress associated with high levels of leverage, which are well known in finance and economics. The large PE firms – the general partners in multiple PE funds – are mainly concerned with acquiring a diversified portfolio of firms, some of which are expected to succeed spectacularly while others may well fail. The relatively low rates of financial distress or bankruptcy among portfolio companies in the years from 1990 to 2007 meant that these failures had little effect on expected returns for the PE funds, and even less for the general partners in these funds, however devastating the effects of distress and restructuring might be for other stakeholders – the managers, workers, and bond holders of the affected operating companies. PE firms assumed that they could safely ignore the risks of financial distress and bankruptcy. In the current period, however, the failure to consider the risks associated with high levels of leverage, particularly as price premiums paid to acquire portfolio companies rose during the bubble years, has had significant consequences for more recent vintages of PE funds. More importantly, operating companies held by PE funds have come under intense pressure. Many are struggling to survive the economic downturn while servicing the high levels of debt with which they are burdened. Refinancing this debt as it matures in today’s very different credit markets poses further challenges. Given these circumstances, many anticipate a wave of bankruptcies in near future that would lead to higher, rather than lower levels of unemployment (Kosman 2009). If, in fact, private equity firms are able to refinance the debt held by portfolio companies, they will need to find others ways of making higher than normal returns, and many have signaled a new strategy of taking a stronger role in restructuring operations and improving performance. The question is whether these strategies will lead to investment in growth activities that will generate employment. Here, existing case studies of private equity firms in the management of operations show that they have more often focused on cost cutting and work intensification rather than long term investment strategies (Appelbaum and Batt 2010). Moreover, given the large body of research on high performance work systems, which show that deep investments and extended time horizons are needed bring about substantial change in operational performance, it is difficult to see how private equity would fulfill this role. An additional question is whether the new financial regulatory reforms will lead to changes in the current business models. In the US, these reforms do not address the fundamentals of the current business models that rely on leveraged debt -- unlike the proposed EU reforms that tackle this issue directly. Moreover, the US regulations do little to curb the private equity business model, with the exception of requiring them to register with the SEC and pay somewhat higher taxes. By contrast, the EU proposals are much more stringent, requiring extensive disclosure and reporting rules, standards for risk management, rules limiting the use of leverage, and anti-money laundering regulations (Batt and Appelbaum 2010). Thus, it is difficult to see how any change in these business models, and their impact on employment, is likely to occur. Appelbaum, Eileen and Rosemary Batt. 2010. “The Challenge of Private Equity: Market Competitiveness and Employment Relations in PE’s Target Companies.” Paper presented at the International Labor Process Conference, Rutgers University, March 13. Batt, Rosemary and Eileen Appelbaum. 2010. Globalization, New Financial Actors, and Institutional Change: Reflections on the Legacy of LEST. Paper presented at the Colloquium: Travail, Emploi et Competence dans la Mondialisation, LEST, Université de la Méditerranée, May 27-28. Appelbaum, Eileen and Rosemary Batt. 2010. “The Risk of Ruin and the PE Model in the Post-Crisis Era.” Working paper. Jacoby, Sanford. 2008. “Finance and Labor: Perspectives on Risk, Inequality, and Democracy,” Comparative Labor Law & Policy 30(17): 17-65. Kosman, Josh. 2009. The Buyout of America: How Private Equity Will Cause the Next Great Credit Crisis. New York: Penguin Group. Lazonick, William. 2009. Sustainable Prosperity in the New Economy. Kalamazoo, MI: W.E. Upjohn Institute. Palley, Thomas. 2007. “Financialization: What It Is and Why It Matters.” Levy Econoimics Institute. Working Paper No. 525. Palley, Thomas I. 2009. America’s Exhausted Paradigm: Macroeconomic Causes of the Financial Crisis and Great Recession, Washington,DC: New America Foundation, June 2009, p. 4. www.newamerica.net/files/nafmigration/Thomas_Palley_Americas_Exhausted_Paradigm.pdf, accessed 4-11-10 Figure 1: Growth of US Debt: 1974-2008

Eileen Appelbaum and Rosemary Batt

Center for Economic and Policy Research and Cornell University |