![]()

![]()

![]()

![]()

Books |

A European Monetary Fund, Recovery and Cohesion

Abstract:

The role recently proposed for a European Monetary Fund is not that of the IMF rather than a debt management institution. Recent multiplier analysis indicates that reducing national debt and deficits without a counter recessionary European recovery programme would have powerfully deflationary effects. It has been recognised since the Amsterdam Special Action Programme that investments in cohesion and competitiveness can be financed by the EIB and other public credit institutions through their own bond issues. But their role needs to be clearly distinguished from any borrowing or debt management by an EMF. Proposals are made for a transfer of a tranche of all member states debt to Union bonds in an EMF which could attract and recycle global surpluses and strengthen both the euro and the single currency area.

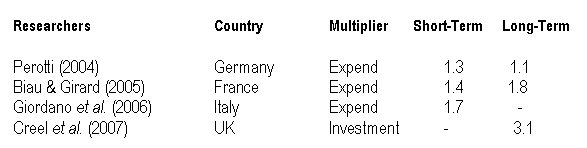

The role recently proposed for a European Monetary Fund is not that of the IMF rather than a debt management institution. Recent multiplier analysis indicates that reducing national debt and deficits without a counter recessionary European recovery programme would have powerfully deflationary effects. It has been recognised since the Amsterdam Special Action Programme that investments in cohesion and competitiveness can be financed by the EIB and other public credit institutions through their own bond issues. But their role needs to be clearly distinguished from any borrowing or debt management by an EMF. Proposals are made for a transfer of a tranche of all member states debt to Union bonds in an EMF which could attract and recycle global surpluses and strengthen both the euro and the single currency area. The declaration by German Finance Minister Wolfgang Schäuble that he would ‘present proposals soon’ for a new eurozone institution that has ‘comparable powers of intervention’ to the International Monetary Fund has been a remarkable feat for Greek Prime Minister George Papandreou. By indicating that he would go to the IMF if there were not assistance for Greece from Europe, he has shifted the whole debate on European economic and monetary union to a new plane. A key issue for the proposed European Monetary Fund is in what way it could reduce excess national debt and protect and enhance the integrity of the single currency area while fulfilling the aim endorsed by the European Parliament for a European Economic Recovery Programme and assuring the commitment of the Union since the Single European Act of 1986 to both an internal market and economic and social cohesion. By contrast what has been suggested to date is exclusively concerned with debt reduction with draconian powers including (1) a suspension of Cohesion Funds; (2) excluding member states from voting in EU Council meetings and (3) proposing a new voting procedure whereby 26 member states would agree to impose such sanctions on another. As well as proposing that Eurozone countries should be barred from applying for assistance the IMF. The Bretton Woods settlement was not that of the Keynes Plan of 1943, but amounted to a stabilisation fund whereby deficit countries would borrow as an alternative to devaluation. Deficit countries should reduce them or be penalised. By contrast there were no sanctions on surplus countries such as the US despite surpluses being the counterpart of such deficits. There are echoes of this in the current EMF proposals. By contrast, the Keynes Plan had been concerned that borrowing should sustain mutual demand, rather than reduce it. Nor did he assume that liberalisation of trade alone would assure full employment, rather than that: ‘The maintenance of employment, on which all our hopes for a permanent liberalization of trading conditions must ultimately rest, requires separate and positive action’. ● Unless proposals for a European Monetary Fund are matched by such ‘separate and positive action’ there will be a massive contraction of mutual spending, trade and employment between member states and not only political dissent but also grave social tensions which could threaten the integrity not only of the single currency but also of the Union. The expenditure and investment multipliers summarised in the table should inform any debate on a European Monetary Fund. They all are estimates of positive multipliers, i.e. the multiplication generated by a given expenditure or investment. But their inverse is negative multipliers.

Multipliers from Public Expenditures and Investments

.● What they imply, and what their authors stress, is that cuts could have multiple negative effects on expenditure from over double to three times their direct impact. The European Economic Recovery programme In principle a two pronged strategy is feasible which is monetarist in the sense of reducing excess debt and deficits - thereby appealing to those for whom this is their major preoccupation - and also Keynesian in the sense of countering the deflationary effects of this with an expansion of investments. An outline of this is given in the attached figure. Thus Structural Reforms would still obtain for Member states in excess of the debt and deficit limits of the SGP, and would reduce them. But this would be countered by EIB investments which mainly are in cohesion areas such as in health, education, urban regeneration and the environment, as well as a reinforcement of competitiveness through the promotion of innovation, green technology and new high-tech start-ups. A simpler move, also in the attached figure, is the ‘tranche transfer’ option whereby a share of all member states’ sovereign debt would be transferred to Union bonds as proposed in the Delors December 1993 White Paper on Growth, Competitiveness, Employment. While not excluding other measures such as regulation of credit default speculation in derivative markets, this would signal to financial markets that the Union would not tolerate a credit default in a member state caused by such speculation. 1. Unlike penalties such as denying access to cohesion funds or suspending a member state from European Councils this would be non-discriminatory. 2. The transfer would not be a debt write-off since member states still would be obliged to service the share of their debt now denominated in € bonds. 3. Whereas loans from an EMF would increase the borrowing of member states in difficulties, the tranche transferred to € bonds would not increase net debt and would be at a lower interest rate spreads than existing national debt. 4. Unlike a Treaty revision, the decision on such a transfer could be taken by the European Council within ‘broad economic guidelines’ for ‘general economic policies’. 5. Pressures to reduce remaining national debt and deficits would be effective since Ecofin could decide on a qualified majority basis - rather than a new voting procedure - that the tranche of national debt transferred to the Union Would be reduced or suspended in the event of member states not making progress in doing so. 6. Expansion of EIB borrowing and national credit institutions to finance the European Economic Recovery programme would mean that there need not be a beggar-my-neighbour contraction of mutual income, employment and trade.

The twin concept, as Delors well grasped, was that (a) the Fund should de facto be a European monetary fund, paralleling the EIB much as the IMF parallels the World Bank and that (b) as with US Treasury debt, its borrowing would not count on that of EU member states. Consideration was given in drafting the proposal that the institution issuing Union Bonds be called a European Monetary Fund. In the final proposal it was not precisely because of the risk - now reflected in the recent proposal for an EMF - that this would encourage a repeat of the deflationary stress of the Structural Adjustment policies of the IMF in the 1980s. There has been scepticism within the Commission and the EIB about the EIF holding and managing new Union bond issues. Until the recent proposal for an EMF this was understandable. The EIF did not embody the original monetary fund design and had been relegated to equity guarantees for small and medium firms. But the new EMF proposal has raised the political stakes and opened new institutional scenarios. If there is to be a European Monetary Fund, yet if this neither is to need a new European institution, nor a Treaty revision, a reconsideration of the original monetary design for the European Investment Fund should be on the agenda. If the EIF were to recover its initial monetary design, this might merit its re-designation as a European Monetary Fund which could be decided by Ecofin. More importantly, its role would need to be clearly defined and as clearly distinguished from that of the EIB, of which more below. But in such a role it could: □ manage the transferred tranche of national debt in Union € bonds; □ accept new investments in such € bonds by sovereign wealth funds and other investors, including European pensions funds; □ recycle these to the EIB and to national public credit institutions; □ thereby make available finance for investments to support the European Economic Recovery Programme which neither would need to be financed only by Commission own resources nor only by European savings. □ strengthen the Eurozone by gaining the euro the role of a global reserve currency.

Earlier re-designation of roles between major European institutions has been achieved by unanimous decision of the European Council without the need for Treaty revisions. For example, on a proposal from then Portuguese Prime Minister Antonio Guterres, the 1997 Amsterdam Special Action Programme invited the EIB to adopt an expanded role through cohesion investments in health, education, urban renewal and the urban environment. The Luxembourg European Council the same year confirmed this. The Lisbon European Council of 2000 then invited the EIB to extend its role to financing investments in technology and innovation. The EIB since has done so with great success in these cohesion areas and in its i2i Investment 2000 Initiative and subsequent Investment 2010 initiative. It has tripled its borrowings and investments and now compares with Commission Own Resources in scale without fiscal transfers or therefore a net cost to any member state. A paper written during the Portuguese Presidency in February 2000 submitted that there was role confusion in finance for SMEs between the EIB, the EIF and the Commission. (Holland, Stuart (2000). "Financing Social Investment, Innovation and Enterprise in the Context of Enlargement". Paper for the Portuguese Presidency of the European Union, February 14th.) An outcome of the paper and a further proposal to the European Council was that, during the Portuguese Presidency, these roles were clarified, with the EIF becoming the venture capital arm of the EIB and the Commission committing itself to more effective coordination of actions to promote SMEs. The September 2008 informal Ecofin decision to authorise the EIB to schedule € 30 billions for this was facilitated by this. If a European Monetary Fund is to be introduced - such as through a role re-designation for the EIF and whether or not with a name change - it nonetheless is vital that such a role should be similarly clear in relation to other institutions, and especially the EIB, as well as national public credit institutions. If its role is to include the issuing of Union € bonds not only in the context of a tranche transfer but also to attract investment in them by pension funds and from sovereign wealth funds it is strongly arguable that it should be restricted to this and recycling them to credit institutions rather than also directly undertaking project finance. ● It is important to clearly distinguish the role of borrowing to invest, as through the EIB or the Marguerite Group of the KfW, the CDC and the Cassa Depositi e Prestiti from debt management. ● It is vital also that the funds of such credit institutions should not be used for salvage operations. Their role is to reinforce and promote success in project finance as the EIB already has been doing with such success in areas directly relevant to both cohesion and competitiveness. The precedents on both role re-designation and clarification by decisions of the European Council indicate that this is entirely feasible without protracted dissent on a further Treaty revision. Stuart Holland

Formerly adviser on European affairs to Harold Wilson, Jacques Delors and Antonio Guterres. Currently Visiting Professor in the Faculty of Economics of the University of Coimbra. His new book "Europe in Question – and what to do about it" is published as an eBook by Spokesman Press and available on Amazon. |